Nacha 2026 Resource Hub

Everything you need to comply, detect, and investigate under Nacha 2026

New fraud monitoring obligations are in effect. Whether you're an RDFI, ODFI, TPS, or TPSP, here's what the rules require and how to meet them.

Effective Date

Mar 20, 2026

Mar 20, 2026

Phase 2 Deadline

Jun 22, 2026

Jun 22, 2026

Volume Threshold

6M+ ACH / yr

6M+ ACH / yr

What Applies to You

Pick your role in the ACH network

Requirements vary by entity type. Select your role to see what's required and how Unit21 helps.

Receiving Depository

Financial Institution

Originating Depository Financial Institution

Third-Party Sender

Third-Party Service Provider

Our Solution

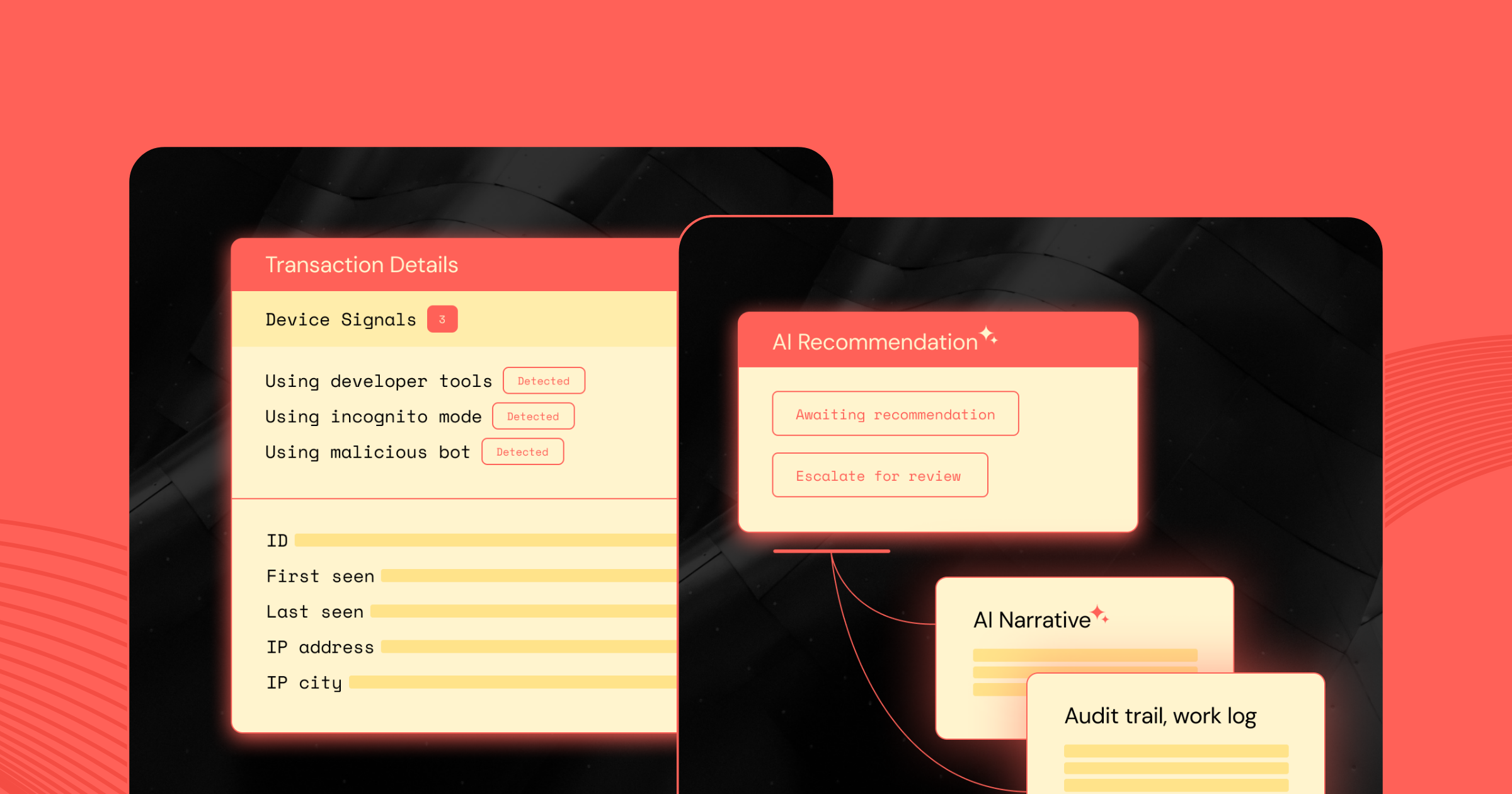

Unit21 helps RDFIs monitor incoming ACH entries using fuzzy name matching, entity-level behavioral rules, and velocity checks, so your team can flag anomalies and act before funds leave the account.

Our Solution

Unit21 lets ODFIs build and deploy risk-based fraud rules for outbound WEB debits without writing code. Flag payroll redirection attempts, BEC patterns, and anomalous origination behavior, with audit-ready documentation for examiner review.

Our Solution

Unit21 gives TPSs the detection infrastructure to monitor ACH transactions originated on behalf of clients. Build originator-level rules, flag anomalous patterns across your client portfolio, and manage alerts through a centralized platform without writing code.

Our Solution

Unit21's platform supports client-level rule customization, behavioral tracking across entities, and centralized case management, giving TPSPs the monitoring infrastructure to meet NACHA's fraud program requirements at scale.

Learn the Rules

Education & References

Practitioner-grade content to understand NACHA 2026 from the ground up. No vendor spin; just what the rules require.

.png)

Unit21 Applied

How Unit21 Can Help

See how to actually implement a NACHA-compliant fraud program inside Unit21: rules, investigations, exam documentation, and all.

Webinar

NACHA 2026 in action: Unit21 does the work, live

NACHA's Phase 2 operating rules hit June 19, 2026, and they change what "reasonable" looks like for every ACH program.

Webinar

Navigating NACHA’s 2026 Operating Rules for ACH Fraud With Unit 21

Join Unit21 in this essential educational session exploring the 2026 NACHA Operating Rules and their implications for fraud monitoring across ACH payments.

.png)

Blog

Building ACH Detection Rules for NACHA 2026: A Step-by-Step Guide for ODFIs and RDFIs

The NACHA 2026 operating rules don't just expand what counts as fraud. They expand what your institution is expected to catch.